![]()

CIMA New 2021 F2 Sample Questions Reliable F2 Test Engine

Feel CIMA F2 Dumps PDF Will likely be The best Option

NEW QUESTION 68

On 1 January 20X7 GH purchased plant and equipment at a cost of $400,000. The temporary differences in respect of this plant and equipment at 31 December 20X7 and 20X8 have been calculated as follows:

Assume that there are no other temporary differences in the periods and that the corporate income tax rate is 25%. GH is expected to have significant taxable profits in the future.

Which of the following is the correct impact in GH's statement of financial position at 31 December 20X8 in respect of deferred tax?

- A. Decrease in the deferred tax asset.

- B. Decrease in the deferred tax liability.

- C. Increase in the deferred tax asset.

- D. Increase in the deferred tax liability.

Answer: C

NEW QUESTION 69

The yield to maturity of a redeemable bond is calculated as the internal rate of return of the relevant cash flows associated with the bond.

Which TWO of the following are considered relevant cash flows in this calculation?

- A. The market value of the bond now.

- B. The redemption value of the bond at the date of redemption.

- C. The annual interest payments net of tax relief.

- D. The nominal value of the bond now.

- E. The value of the conversion premium on conversion to equity shares.

Answer: A,B

NEW QUESTION 70

FG has a weighted average cost of capital of 12% based on its existing:

* level of gearing of 30% (measured as debt/(debt + equity)); and

* business operations.

This would be used as an appropriate discount factor to assess which of the following significant projects?

- A. A project in an industry in which FG does not currently operate, funded wholly by equity.

- B. A project to extend FG's existing operations, funded wholly by debt.

- C. A project in an industry in which FG does not currently operate, funded 30% with debt and 70% with equity.

- D. A project to extend FG's existing operations, funded 30% with debt and 70% with equity.

Answer: D

NEW QUESTION 71

Entity A entered into a 3 year operating lease on 1 April 20X3. The rentals are £5,000 a year payable in advance with an additional payment of $1,800 payable on 1 April 20X3.

The rental expense to be included in the statement of profit or loss for the year ended 31 December

20X3 will be:

- A. $6,800

- B. $4,200

- C. $5,600

- D. $5,000

Answer: B

NEW QUESTION 72

GH is seeking to finance a substantial new project that is guaranteed to enhance the profitability of the entity. Its key determinants in deciding upon the best source of finance are to balance the following requirements:

1) to minimise the costs of issue of the finance;

2) to avoid the need to find cash to repay the source of finance; and

3) to ensure that the long-term gearing level does not increase.

Which of the following financing options best meets these requirements?

- A. Redeemable preference shares

- B. Convertible loan stocks

- C. A term loan

- D. Initial public offering of ordinary shares

Answer: B

NEW QUESTION 73

Information from the financial statements of RST for the year ended 30 April 20X9 is as follows:

At 30 April 20X9 the ordinary shares are trading at $4.75.

What is the price earnings (P/E) ratio for RST at 30 April 20X9?

- A. 15.83

- B. 9.31

- C. 10.56

- D. 7.92

Answer: A

NEW QUESTION 74

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years' time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classified as which of the following?

- A. Compound instrument

- B. Debt instrument

- C. Equity instrument

- D. Discounted instrument

Answer: A

NEW QUESTION 75

What is the total comprehensive income attributable to the non-controlling interest that will be presented in GHI's consolidated statement of changes in equity for the year ended 31 December 20X4?

- A. $595,000

- B. $95,000

- C. $190,000

- D. $575,000

Answer: B

NEW QUESTION 76

On 30 November 20X9 OPQ acquires a financial asset that is classified as Available for Sale.

Which of the following describes the value of the financial asset on the date of acquisition?

- A. Fair value including transaction costs.

- B. Present value including transaction costs.

- C. Present value excluding transaction costs.

- D. Fair value excluding transaction costs.

Answer: A

NEW QUESTION 77

What is meant by the term "a placing of ordinary shares"?

- A. Selling new ordinary shares to existing shareholders.

- B. Selling new ordinary shares directly to the public.

- C. Selling new ordinary shares to a financial institution on a pre-arranged basis.

- D. Selling existing ordinary shares to new investors through a stock exchange.

Answer: C

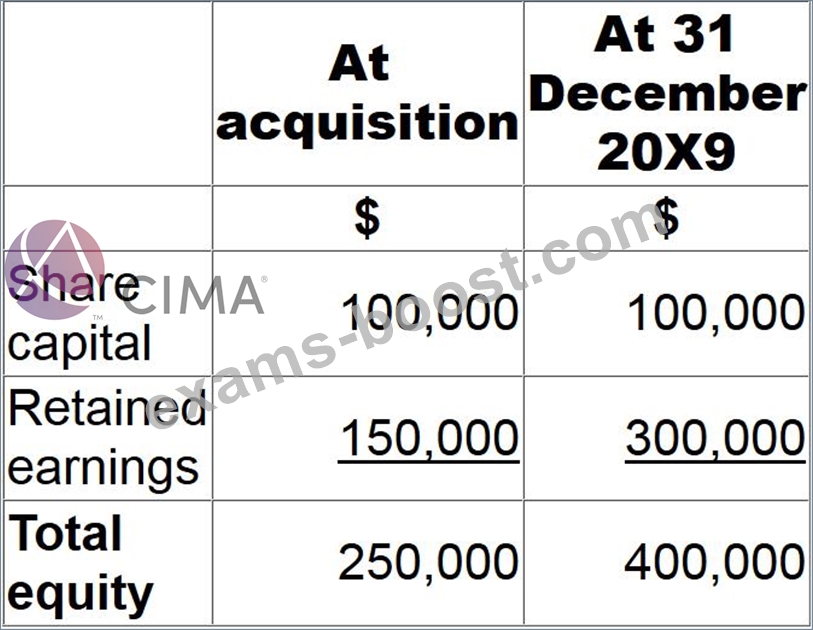

NEW QUESTION 78

ST owns 75% of the equity share capital of GH. GH owns 80% of the equity share capital of RS.

The following balances relate to RS:

The non controlling interest in respect of RS had a fair value of $56,000 at acquisition. There has been no impairment to goodwill since acquisition.

What value should be included in ST's consolidated statement of financial position for the non controlling interest in RS at 31 December 20X9?

- A. $116,000

- B. $93,500

- C. $86,000

- D. $146,000

Answer: A

NEW QUESTION 79

Which of the following would limit the effectiveness of analysis performed on the operating profit margins of two separate entities with the same total revenue over a12 month period?

- A. Different pattern of monthly revenues caused by seasonality.

- B. Different accounting estimates in respect of depreciation of property, plant and equipment.

- C. Different approaches to allocating expenses to cost of sales, administration expenses and distribution costs.

- D. Different interest rates on loan finance available to the entities.

Answer: B

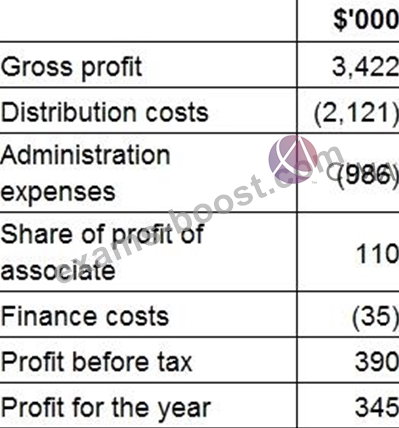

NEW QUESTION 80

At 31 October 20X1 RS has in issue 10% debentures 20X8 with a carrying value of $350,000.

Extracts from its statement of profit or loss for the year ending 31 October 20X7 are as follows:

What is the interest cover for RS for the ended 31 October 20X7?

- A. 11.1 times

- B. 9.0 times

- C. 10.0 times

- D. 8.0 times

Answer: B

NEW QUESTION 81

Which THREE of the following statements about preference shares are true?

- A. Preference shareholders rank below the equity shareholders in a winding up.

- B. Unlike ordinary shares, preference shares may be cumulative.

- C. The characteristics of preference shares are closer to debt than equity.

- D. For an investor, preference shares carry more risk than ordinary shares.

- E. Preference shareholders receive their dividend entitlement before the equity shareholders.

- F. Preference shares cannot be issued as redeemable shares.

Answer: B,C,E

NEW QUESTION 82

JKL measure gearing as debt:equity, based on book values. At 31 December 20X5 the ratio is 2:3 and JKL would like this to be 2:5.

Which of the following transactions individually would achieve this?

- A. Bonus issue from the share premium account.

- B. Revaluation of investment property to an increased fair value.

- C. Issue of redeemable preference shares at par.

- D. Repayment of a 6 year term loan with the issue of 5 year redeemable debentures.

Answer: B

NEW QUESTION 83

Which of the following would cause a deferred tax balance to be included in the statement of financial position for an entity?

- A. The acquisition of land for which there is no tax depreciation.

- B. The acquisition of plant and equipment a year ago where the tax depreciation rate is different to the accounting depreciation rate.

- C. Impairment of goodwill that arose on the acquisition of a subsidiary entity.

- D. Expenses in the statement of profit or loss which are not allowable for tax creating a permanent difference.

Answer: B

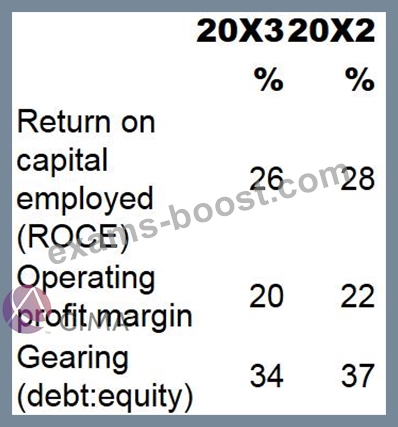

NEW QUESTION 84

Ratios have been produced below for EF for the year to 31 March:

Which TWO of the following could explain the movement in both gearing and ROCE?

- A. A revaluation upwards on the head office property on 1 April 20X2.

- B. A rights issue on 31 March 20X3.

- C. A bonus issue of shares on 1 April 20X2.

- D. A bank loan to purchase new machinery on 31 March 20X3.

- E. A debt issue on 31 March 20X3.

Answer: A,B

NEW QUESTION 85

GH's financial statements show the following:

What is the value of the dividend received from the associate to be included in GH's consolidated statement of cash flows for the year?

Give your answer to the nearest $000.

$ ? 000

Answer:

Explanation:

300, 300000

NEW QUESTION 86

When preparing a consolidated statement of cash flows, which of the following describes the correct presentation of an associate's dividends?

- A. Dividends paid by the associate in cash flows from financing activities

- B. Dividends received from the associate in cash flows from investing activities

- C. Dividends paid by the associate in cash flows from investing activities

- D. Dividends received from the associate in cash flows from operating activities

Answer: B

NEW QUESTION 87

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease.

AB used the cash proceeds from the sale to reduce its long term borrowings significantly. No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB's ratios calculated at 31 December 20X9?

- A. AB's return on capital employed would be lower as a result of this sale being recorded.

- B. AB's current ratio would be lower as a result of this sale being recorded.

- C. AB's non-current asset turnover would be lower as a result of this sale being recorded.

- D. AB's gearing ratio would be lower as a result of this sale being recorded.

Answer: D

NEW QUESTION 88

Which TWO of the following are true in relation to IAS21 The Effects of Changes in Foreign Exchange Rates when consolidating an overseas subsidiary?

- A. Assets and liabilities of the subsidiary are translated at each reporting date using the average exchange rate for the period.

- B. Goodwill is reflected in the consolidated statement of financial position translated at the exchange rate on the date of acquisition.

- C. A current period exchange gain or loss is shown within the consolidated statement of comprehensive income within other comprehensive income.

- D. Goodwill is re-translated at the end of each reporting period and reflected at the period end exchange rate in the consolidated statement of financial position.

- E. The statement of profit or loss of the subsidiary is translated for the reporting period using the closing exchange rate.

Answer: C,D

NEW QUESTION 89

XYZ had 600,000 ordinary shares in issue on 1 July 20X4. On 1 January 20X5, the entity made a 1 for 2 bonus issue. The profit attributable to ordinary shareholders for the year ended 30 June 20X5 was

$2,925,000.

What is the basic earnings per share for the year ended 30 June 20X5?

- A. $1.63

- B. $3.25

- C. $3.90

- D. $4.88

Answer: B

NEW QUESTION 90

An investor owns 75 shares values at $1.50 each. If the shares increase in value to $1.75, how much money will the investor have made through this capital gain?

- A. $131.25

- B. $187.50

- C. $26.25

- D. $18.75

- E. $112.50

- F. $15

Answer: D

NEW QUESTION 91

When establishing a group structure, which of the following factors need to be considered: Select ALL that apply.

- A. Non-controlling interests

- B. The percentage ownership

- C. Whether control is direct or indirect

- D. Whether control has been established

- E. Goodwill

- F. The date of acquisition

- G. Intra-group investments

Answer: B,D,F

NEW QUESTION 92

......

Use Valid New F2 Test Notes & F2 Valid Exam Guide: https://www.exams-boost.com/F2-valid-materials.html